There’s a term I’ve started using to describe today’s real estate market:

The Housing Logjam.

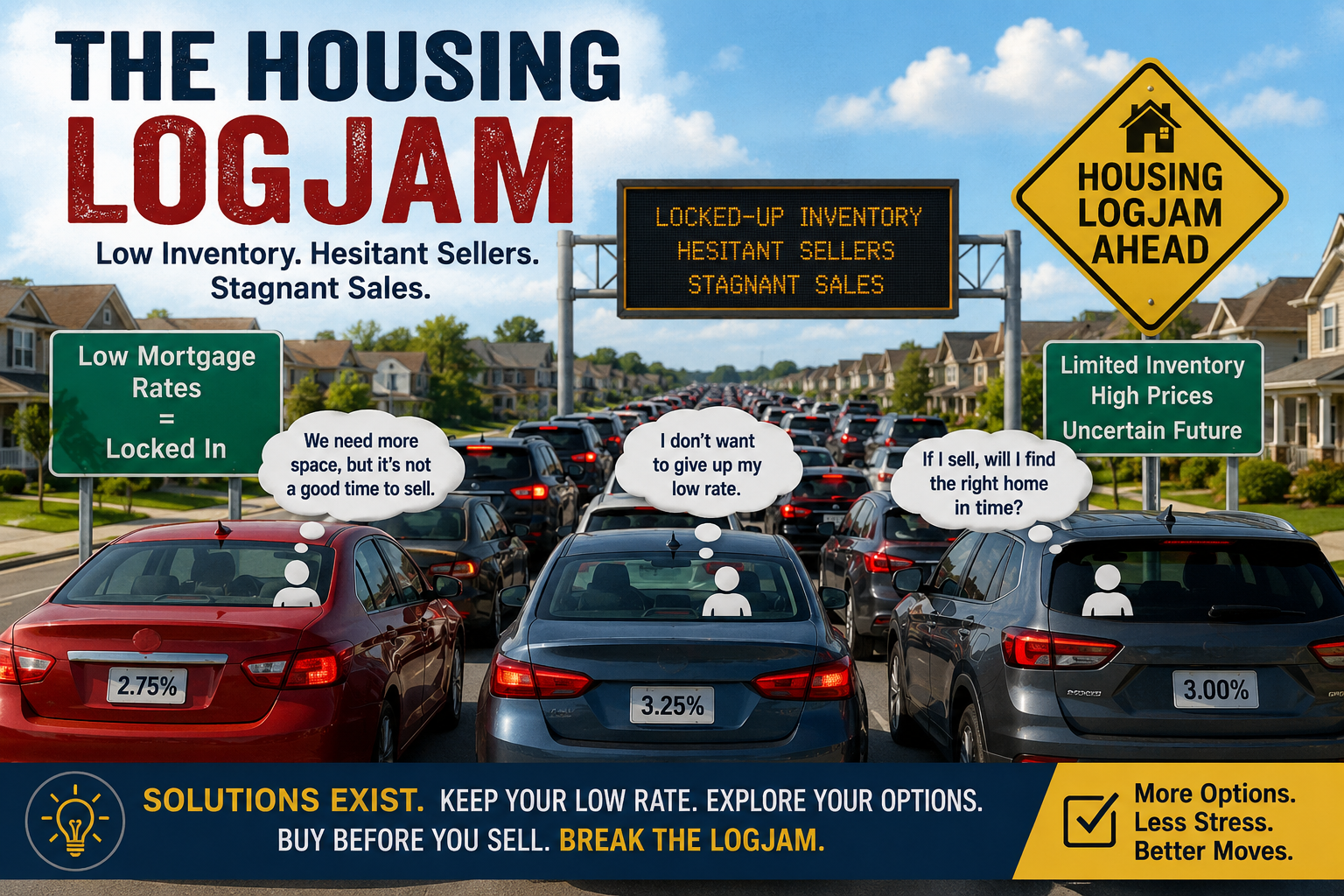

It’s the perfect way to describe what’s happening with locked-up inventory, hesitant sellers, and stagnant home sales across many markets.

And honestly, it makes sense.

Homeowners are sitting on historically low mortgage rates that may never be seen again in our lifetime. Many refinanced or purchased homes with interest rates well below today’s market rates, and understandably, they’re reluctant to let those loans go.

During annual mortgage reviews with clients, I hear comments like:

“I’m not selling unless buyers make it worth giving up my low rate.”

Or:

“We need more space, but the market feels flat. It’s probably not a good time to sell.”

Ironically, if prices are flatter or softer, wouldn’t that also make it a potentially good time to buy—especially if you’re moving up into a larger home?

But emotions, uncertainty, and logistics often keep people frozen in place.

And even for homeowners who want to sell, another concern quickly surfaces:

“If I sell my current home, will I actually find another home quickly enough? Or will I end up stuck renting for a year?”

That fear alone keeps many would-be sellers from listing their homes.

The result?

A housing market where:

- Buyers struggle with limited inventory

- Sellers hesitate to move

- Transactions slow down

- Everyone waits for someone else to make the first move

That’s the housing logjam.

First Option: Don’t Sell at All

Sometimes my first recommendation is surprisingly simple:

Don’t sell. Keep the home.

For many homeowners, especially those with:

- Interest rates below 5%

- Low mortgage balances

- Significant equity

- Strong rental demand in their area

…their current home may actually make an excellent investment property.

With such a low cost basis, homeowners may be able to:

- Generate positive cash flow

- Remain competitive with rental pricing

- Attract strong tenants

- Maintain lower vacancy rates

And recent underwriting guideline changes have made retaining a departing residence more realistic for many borrowers than in years past.

Of course, owning investment property isn’t for everyone, and not every home is ideally suited as a rental. But it’s absolutely worth discussing with a trusted Mortgage Professional and Real Estate Agent before automatically deciding to sell.

Still, while that strategy may help individual homeowners, it doesn’t necessarily solve the larger housing logjam.

The Bigger Solution: “Buy Before You Sell”

Now here’s where things get really interesting.

A growing number of homeowners may qualify for programs designed to let them buy their next home before selling their current one.

At first glance, most people respond with:

“How is that even possible?”

It’s a fair question.

Most homeowners assume they cannot qualify carrying two mortgage payments at once—or that they absolutely need the equity proceeds from their current home before purchasing another property.

But recent underwriting changes and specialized financing programs have made this possible for more borrowers than ever before.

And the benefits can be significant.

Why “Buy Before You Sell” Changes Everything

Think about all the stress points this strategy can eliminate:

No Contingency Offers

Sellers often reject offers contingent on another home selling first. Buying before selling can make your offer far more competitive.

No Family Disruption

You avoid constant showings, last-minute cleaning, and rearranging your life around buyers walking through your home.

No Pressure to Accept a Low Offer

Without looming deadlines, sellers can wait for stronger offers instead of feeling forced into price reductions.

No Rushed Buying Decisions

You gain time to find the right home instead of settling because the clock is ticking.

No Temporary Housing

No lease-backs. No short-term rentals. No living out of boxes.

No Moving Twice

One move. One transition. Much less stress.

More Control Over the Timeline

This may be the biggest benefit of all. Homeowners regain flexibility and decision-making power.

Additional Benefits Most Sellers Don’t Think About

The advantages don’t stop there.

Many “Buy Before You Sell” programs also allow:

- Access to a portion of your current home equity before selling

- Potential exclusion of the departing residence payment from debt calculations

- Greater flexibility during underwriting

And there’s another major advantage:

Vacant Homes Often Sell Faster—and for More

Once a homeowner moves into their new property, they have the opportunity to:

- Declutter

- Neutralize décor

- Make minor updates

- Professionally stage the home

And let’s face it—buyers don’t always share the same decorating tastes.

Even beautiful homes can become harder to sell when buyers can’t see past bold colors, personal décor, or cluttered spaces.

Neutral, vacant homes often appeal to a larger pool of buyers, show better, and can sometimes command stronger offers.

Will This Completely Break the Housing Logjam?

Maybe not completely.

But it may help loosen it.

The more flexibility homeowners have, the more willing they may become to move, upgrade, downsize, or make lifestyle changes they’ve been postponing.

And that creates movement.

Movement creates inventory.

Inventory creates opportunity.

If you’ve been feeling stuck because you’re unsure how to navigate selling and buying simultaneously, it may be worth exploring whether a “Buy Before You Sell” strategy could work for you.

The right loan program, combined with the right Real Estate Agent and Mortgage Professional, can dramatically reduce stress and create more options.

And when it comes to buying or selling a home, more options are almost always a good thing.

It’s still a great time to buy—and with the right strategy, it may also become a much easier time to move.

Jay Atterstrom

📧 [email protected]

📞 (214) 377-0033